Condo vs. Freehold in Ontario: Which Is the Smarter Buy in 2026?

First-time buyers face a pivotal choice: condo vs. freehold in Ontario 2026. Here's what the numbers say about prices, monthly costs, and long-term value.

The Question That Defines Your First Decade of Ownership

For most first-time buyers in Ontario, this is the decision. Not which neighbourhood. Not which realtor. Not even which mortgage product. It's the condo vs. freehold question, and it shapes everything that follows: your monthly costs, your maintenance responsibilities, your resale trajectory, and honestly, your daily quality of life.

In 2026, the calculus has shifted in ways that weren't true three years ago. Condo prices have softened significantly while freehold has held up better. New mortgage stress test rules and rising rates are making buying power tighter. And a wave of investor-owned condo inventory is flooding certain GTA submarkets, creating both opportunity and risk depending on how you look at it.

This guide breaks down the real differences—not the theory, but the actual numbers, the actual trade-offs, and a practical framework to help you decide which type of property makes sense for where you are right now.

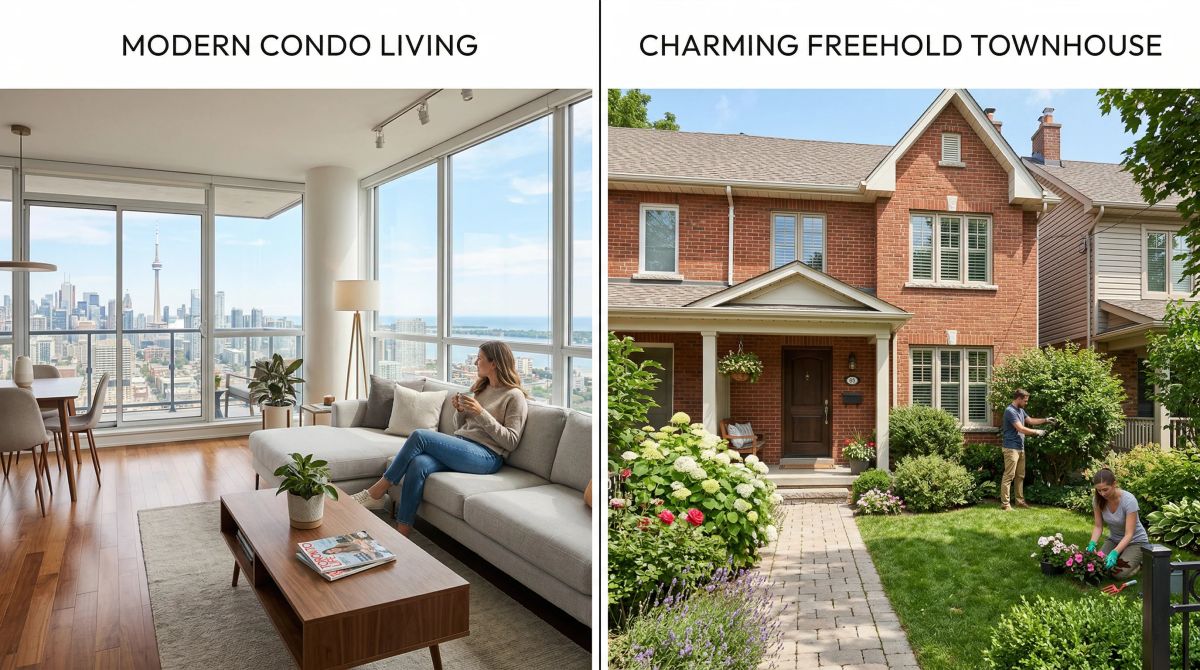

What Each Type Actually Means

It's worth being precise here because the terminology gets muddled.

Freehold ownership means you own both the land and the structure on it. Most detached houses, semi-detached homes, and freehold townhouses fall into this category. You own the driveway, the yard, the foundation, the roof. When something breaks, it's your problem and your expense. When you want to renovate, you can (subject to permits and local bylaws). You're not accountable to a condo corporation, and there's no monthly maintenance fee that someone else sets.

Condo ownership means you own your individual unit plus an undivided share of the building's common areas—the lobby, hallways, gym, parking structure, roof, and mechanical systems. A condo corporation governs the building, managed by a board (usually elected from among unit owners) and a property management company. You pay monthly condo fees to fund building operations and the reserve fund. In exchange, you don't shovel snow, fix the roof, or repair the elevator. The condo corporation handles all of that.

Condo apartments and condo townhouses are both governed this way. The distinction matters when it comes to costs, control, and lifestyle.

Where Prices Actually Stand in February 2026

Let's put some numbers on the table. According to WOWA's February 2026 GTA housing market data, average sold prices by property type looked like this:

GTA Average Sold Prices – February 2026

Detached: $1,325,654 (down 8.3% year-over-year)

Semi-Detached: $1,027,376 (down 4.9% year-over-year)

Freehold Townhouse: $930,779 (down 6.1% year-over-year)

Condo Apartment: $626,650 (down 8.9% year-over-year)

Condo Townhouse: approximately $749,000

The GTA benchmark home price across all property types sits at $938,800, down 7.9% year-over-year. The market is firmly in buyer's territory, with roughly five months of supply—anything above five months is considered a buyer's market.

What these numbers tell you: condos are the most affordable entry point by a substantial margin. A $627K average for a condo apartment vs. $931K for a freehold townhouse is a $304,000 gap. On a 20% down payment, that's $61,000 more cash required just to get into the freehold. For many first-time buyers, that gap is the entire conversation.

Monthly Cost Comparison: $650K Condo vs. $950K Freehold Townhouse

Let's run a realistic side-by-side comparison using current market assumptions. 20% down payment, 25-year amortization, fixed rate of approximately 4.7% (reflecting recent increases).

$650,000 Condo Apartment

Down payment (20%): $130,000

Mortgage: $520,000

Monthly mortgage payment: ~$2,920

Condo fees (GTA average): ~$650–$800/month

Property tax (estimated): ~$275/month

Insurance: ~$75/month

Total monthly cost: approximately $3,920–$4,070

$950,000 Freehold Townhouse

Down payment (20%): $190,000

Mortgage: $760,000

Monthly mortgage payment: ~$4,265

Maintenance reserve (self-managed): ~$200–$300/month

Property tax (estimated): ~$425/month

Insurance: ~$150/month

Total monthly cost: approximately $5,040–$5,140

The condo comes in roughly $1,000–$1,200 per month cheaper in carrying costs. That's real money. But the comparison has an asterisk: condo fees are not static. They tend to rise 3–5% per year, and special assessments can add sudden large lump-sum costs. The freehold's maintenance budget, on the other hand, is more predictable because you control it—though major repairs (roof, furnace, foundation) can hit without warning.

The Condo Market in 2026: Opportunity With Asterisks

The condo market right now is genuinely complicated, and buyers need to understand both sides of it.

The opportunity: prices have come down significantly. Condo apartments in the GTA are averaging $627K—roughly 8.9% below where they were a year ago, and near multi-year lows. For a first-time buyer who's been waiting for affordability to improve, this is the moment. You can buy a well-located condo in a building that was out of reach two years ago at a price that actually pencils out against the rental alternative.

The challenge: investor exodus and oversupply. The condo market swelled with investor-owned units during the low-rate era, and a significant portion of those investors are now exiting—either because their properties are cash-flow negative, or because they're facing mortgage renewals they can't afford. That's added to already-elevated inventory levels, and it's keeping resale prices under pressure. According to Reddit's TorontoRealEstate community, months of inventory for condos has risen to as high as 6.7 in some periods—deeply in buyer's market territory.

The practical implication: if you're buying a condo to live in, the current pricing is favourable. If you're buying primarily as an investment with plans to rent it out, the numbers are much harder to make work right now. Monthly carrying costs frequently exceed achievable rents in many buildings, meaning negative cash flow from day one.

Freehold: The Advantages Are Real

Freehold ownership has held its appeal for good reasons, and in 2026, several of those reasons are more compelling than ever.

No condo fees: There's no monthly obligation to a corporation. Your maintenance costs are whatever you decide to spend and when. If the roof is fine, you spend nothing this month. If you want to renovate the kitchen, you decide when, what, and how much. That autonomy has real financial value.

No special assessments: Condo buildings can—and do—levy special assessments when the reserve fund is underfunded. These can run from a few thousand to tens of thousands of dollars per unit, and they're often difficult to predict when you're buying. The O'Reilly Group makes this point clearly: with a freehold, you won't suddenly receive a bill because there wasn't enough money in the reserve fund to replace the roof. You are the reserve fund.

Historically stronger appreciation: Freehold properties—particularly detached and semi-detached homes in the GTA—have generally outperformed condos in appreciation over rolling 10-year periods. Land is the scarce resource; condos can always be added to the supply. This isn't a guarantee, but it's a consistent pattern in Toronto's market history.

Freedom to renovate: Want to knock down a wall, build a deck, add a rental suite in the basement? With a freehold, the decisions are yours. Condo bylaws restrict everything from flooring choices to whether you can have a BBQ on your balcony.

Freehold: The Trade-Offs You Need to Know

The higher entry price is obvious—$190,000 down vs. $130,000 down in the comparison above. But the less-discussed disadvantages matter too.

All maintenance falls on you: There's no property manager to call when the furnace dies at 6am in January. There's no superintendent to deal with a water heater issue. You either fix it yourself or you pay someone to fix it—on your timeline, at your expense. The conventional wisdom is to budget 1–2% of your home's value annually for maintenance. On a $950,000 home, that's $9,500–$19,000 per year. In practice, some years you spend almost nothing; in others, you might replace the HVAC, re-side the garage, and re-do the driveway.

Higher carrying costs from day one: The mortgage on a freehold is substantially larger, which means more of your monthly income goes to debt service. This can be constraining in ways that affect other life goals: saving for retirement, taking parental leave, changing careers.

Neighbour dependency: Semi-detached homes and freehold townhouses share walls with neighbours. You don't pay condo fees, but the person attached to your home makes choices that affect your property—how they maintain their unit, what they do to the shared fence or roof. The O'Reilly Group notes that the lack of formal governance can actually be a disadvantage in these situations, because there's no condo board to enforce standards.

Condo: The Advantages Buyers Often Overlook

Lower purchase price is the headline advantage, but condos have genuine lifestyle benefits that suit a lot of buyers perfectly.

Maintenance-free living: Snow removal, lawn care, exterior maintenance, building systems—all handled. For single professionals, frequent travellers, or anyone who just doesn't want to spend weekends managing property, this is significant. You own real estate without owning its problems.

Amenities you'd otherwise pay for separately: Many GTA condo buildings include gym access, concierge, rooftop terraces, party rooms, and visitor parking. If you'd be paying for a gym membership anyway, that $100/month is already partially embedded in your condo fees.

Location advantages: Condos are almost exclusively concentrated in the most transit-accessible, walkable urban neighbourhoods. The same $627,000 that gets you a condo in Liberty Village or the Annex will not get you a freehold property anywhere close to downtown Toronto. For buyers who prioritize walkability, commute time, and urban amenity access, the condo is often the only realistic option at that price point.

Condo: The Disadvantages You Can't Ignore in 2026

Fees that always go up: Condo fees have one direction of travel. A $650/month fee in year one is likely $750–$800 by year five. Boards can also raise fees sharply if the reserve fund is depleted or if unexpected capital expenditures arise. You have a vote at the AGM, but you're ultimately subject to what the majority decides.

Resale challenges in the current market: With condo inventory elevated and investor units continuing to hit the market, resale timelines are longer and price concessions are more common than they were two or three years ago. Months of condo inventory in the GTA have hit levels not seen since the early 2010s. This doesn't mean condos are a bad investment, but buyers should enter without expecting quick appreciation.

Less control over your home environment: You can't rent on Airbnb if the building doesn't allow it. You can't renovate the lobby, add a storage unit, or change the parking allocation. You can't prevent a noisy tenant from moving in two floors below you. You're part of a community, which is great until the community makes decisions you disagree with.

The Stepping Stone Strategy: Does It Still Work in 2026?

For years, the conventional wisdom for Toronto first-time buyers went like this: buy a condo, build equity over five years, use that equity as a down payment on a freehold. Simple, logical, reliable.

Does it still work? The honest answer is: it depends on where you buy and at what price.

If condo prices stay flat or continue to slide over the next five years while freehold prices remain relatively stable, you'd be building equity on a depreciating asset and trying to step up to a market that hasn't corrected proportionally. The math gets messy.

On the other hand, buyers who purchased condos at current low prices and hold through a market recovery could see solid gains. And the carrying cost savings—roughly $1,000/month vs. a freehold—can be aggressively redirected into the mortgage or savings, accelerating the path to a larger down payment.

The stepping stone strategy works best when: you buy at a price that genuinely represents value (today's condo market largely qualifies), you hold for at least five to seven years, and you buy in a building with strong fundamentals—healthy reserve fund, low vacancy, good management, and a location with long-term demand.

It works less well when: you buy purely for appreciation in a soft market, you choose a building based on amenities without reviewing the status certificate, or you plan to sell in two to three years and expect to time the market perfectly.

The Decision Framework: Which One Is Right for You?

Work through these questions honestly and the answer usually becomes clear:

Budget: Can you genuinely afford the down payment and carrying costs of a freehold at current prices without stretching dangerously? If the answer is no without significant compromise on location or quality, the condo isn't a consolation prize—it's the right financial decision.

Lifestyle: Do you value autonomy and space, or convenience and low-maintenance living? If you're a DIYer who wants a garden, a freehold is probably a better fit. If you travel frequently, live alone, and hate yard work, a condo may serve you far better.

Timeline: Are you planning to stay for at least five to seven years? That's the minimum threshold for a real estate purchase to be financially sound in most scenarios. If you're uncertain about your timeline—new job, possible relocation, relationship changes—a condo typically offers more flexibility on the exit.

Investment horizon: Do you prioritize long-term appreciation potential and land ownership? Freehold wins that argument historically. Do you need the lower entry point to get into the market at all? The condo opens the door.

Risk tolerance: Special assessments, rising condo fees, and building management quality are all variables you can't fully control in a condo. Unexpected major repair bills are variables you can't fully control in a freehold. There's no risk-free option. The question is which kind of uncertainty you're better equipped to manage.

In 2026, both options have genuine merit and real trade-offs. The condo market offers its best pricing in years. The freehold market offers long-term stability and ownership clarity. Neither is the automatic answer. But for buyers who've been waiting on the sidelines, the current conditions—elevated inventory, buyer-friendly market dynamics, and slightly lower rates than the peak—represent a window that's worth taking seriously before it closes.

Written by

Sara Shao

Senior Buyer Specialist

Mandarin- and English-speaking GTA buyer specialist with 10+ years guiding first-time home buyers, new immigrants, and condo investors across Markham, Scarborough, and Richmond Hill.

View all articles by Sara →